Business Sectors

Events

Contents

Demand for cleaner energy driving LNGC orderbook and retrofits

There are exciting LNGC orders on the horizon and now demand for LNG as a marine fuel is developing a healthy retrofit sector, too

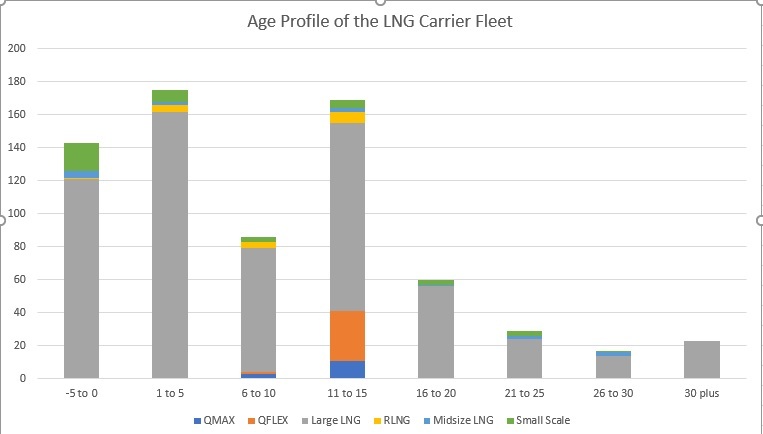

The LNG carrier (LNGC) fleet passed a new milestone in 2019 when the five hundredth vessel hit the water, reflecting the astonishing growth in this sector which has mirrored growing demand for LNG in developed and developing countries. Over the last four decades, seaborne trade in LNG has grown from 52M tonnes at the end of the 1980s to 93M tonnes at the end of the 1990s. The 2000s saw a doubling of demand for seaborne LNG to 183M tonnes. The growth of Chinese demand for seaborne LNG in the 2000s was a driving force behind its growth to 351M tonnes. The Chinese economy may be slowing as it matures, but LNG demand continues to increase. In the 2000s Chinese imports (all goods and services) grew by around 18% per year, but since 2015 this has slowed to around 5% per year, apart from LNG imports which, according to Clarkson Research Services (CRS), were up 16% in 2019.

This is putting some welcome strain on the fleet, with the LNGC utilisation rate set to remain elevated over the next couple of years, according to shipping consultancy Maritime Strategies International (MSI). MSI feels that the LNG sector is poised for further periods of high spot and short-term charter rates, but the industry is at an inflexion point. The vast bulk of the LNGC fleet is currently under 15 years old, but decisions have to be made now if that profile is to be maintained for the first half of the next decade and beyond.

Demand growth is fuelling demand for LNGCs, with over 50 newbuilding contracts placed in 2019. All but five contracts were for large LNG carriers in the 100,000 to 199,999 m3 range, the vast majority being around 174,000 m3. According to VesselsValue figures, Daewoo won 10 174,000 m3 LNGC contracts, Hudong Zhonghua won four, Hyundai Heavy Industries won 12, Hyundai Samho won seven, and Samsung Heavy Industries won 13. These will bolster the Large LNG sector which already contributes 84% to the whole of the LNG fleet. The increase in demand for Large LNG carriers in 2019 came against a background in increasing prices. According to CRS, the 174,000 m3 newbuilding price in 2018 was US$182M and rose to US$186M by the end of 2019. CRS also noted in a recent paper that there is strong order potential for 2020; no names were given, but it would be easy to speculate on possible orders.

Ice-class LNGCs

Top of the list of potential new shipbuilding contracts would be a fleet of ice-class LNGCs to service the Russian Novatek Arctic LNG 2 project. A report by Business Korea noted South Korean shipbuilder Samsung Heavy Industries was in the running to win the order to build 10 Russian Register Arc7 class for year-round operation. The vessels are be built in parallel with five units constructed at Russia’s Zvezda Shipyard. The Russian yard would build a pilot vessel using GTT’s newly developed Arctic version of the Mark III Flex tested at the Krylov State Research Centre in St Petersburg, Russia. The cost of each vessel would be around US$300M. It has been reported that the first vessel is due Q1 2023, so an announcement on the contract seems imminent.

That said, there remains the question of yard capacity. According to Golar LNG, a contract placed in 2020 for a Large LNG carrier would be given a delivery date of H2 2022. By then the LNGC fleet might be in negative demand territory. Contrast this with 2015, when there were an estimated 29 LNGC in excess of supply (Fearnley LNG figures); by 2019, this had reduced to just six vessels. According to Golar LNG, by the end of 2020 there might be a deficit of supply by 11 vessels. In addition to the Large LNG carriers due for delivery in 2020, only six are not committed to long-term projects or charters. This could result in something of a rate bonanza in the LNGC spot market, which in itself might trigger a new round of speculative ordering.

While the LNGC fleet continues to grow in size and sophistication, according to some estimates, around 20% of the fleet is ‘commercially challenged’ by having smaller cargo capacity and higher fuel consumption engines. GasLog Ltd estimates that the steam-powered portion of the Large LNG carrier fleet has an average debt of less than US$60M per vessel, compared to twice that level for a modern TFDE (more for an X-DF-engined Large LNGC). The ability of these near-debt free vessels to find cargoes at times of peak demand is a drag on the spot market. Only three Large LNGCs were scrapped in 2019, the 1981-built Pacific Energy, the 1977-built Sunrise, and the 1980-built Mourad Didouche. The French-built Sunrise’s specification included a design speed of 22 knots and heavy fuel oil consumption of 220 tonnes per day!

A younger vessel might warrant being re-engined to dual-fuel capability, an increasingly popular option for newbuildings, and not just for LNGCs. According to CRS around 30% of orders across 2019 were LNG-fuel capable. Stripping out the LNGC orders, this share was around 17%, increasing to 25% for those orders announced in December alone. 2019 saw the first dual-fuel LNG orders for a VLCC (at DSIC), a Suezmax (GSI), a Capesize (HHI) and a Newcastlemax (SWS).

The box marked ‘LNG-power’ when ordering a newbuilding is likely to become a more popular option, as shipping struggles with its commitment to a greener profile. Shipping needs to deal with its 850M tonne CO2 footprint (approximately 2.4% of global output) in a way that acknowledges that current vessels that will be comfortably within a normal lifespan in 2030 and even 2040. But it is not cheap. Publicly listed COSCO Shipping Energy Transportation (CSET) of China reported that it will pay an additional US$6M for one of its VLCCs on order at Dalian Shipbuilding to be re-specified with LNG dual power. The design of the dual-fuel LNG-powered VLCC is based on rules agreed in principle with DNV GL in 2015. However, it appears that this price did not include state subsidies and the ‘real’ premium is around US$15M.

: A fan of LNG but feels VLCC LNG retrofits are a step too far")

Retrofits

But what about retrofitting LNG dual-fuel engines on vessels? This is an increasingly popular option, and is the approach taken by Tote. According to DNV GL’s Alternative Fuel Insight Platform (AFI) database, 23 vessels have bene retrofitted with LNG fuel engines. A key influencer in the retrofit process is the size of the LNG tank. The largest LNG tank fitted so far in a retrofit is the 6,500 m3 tank installed on the UASC containership Sajir. Many regard the LNG retrofit on the 2014-built 15,000 teu vessel as a pilot study for the whole of the shipping industry.

Sajir had been built in 2014 with the possibility of introducing LNG, but even so, it was not a straightforward process. Owner Hapag-Lloyd said without the pre-retrofit work, its investment for the conversion would have bene a lot higher, as it can cost US$1M for just one auxiliary to be modified to a dual-fuel engine.

Furthermore, MAN head of sales, retrofit projects Klaus Rasmussen says Hapag-Lloyd paid a higher cost for the retrofit work on Sajir because it was first of its kind. He says any further retrofits would be cheaper a result of this work. The vessel’s 54.9-MW MAN B&W 9S90MEC10 engine was converted to MAN Energy Solutions’ dual-fuel ME-GI engine concept.

To date, nine vessels have had engines converted to WinGD’s dual-fuel LNG burning DF engines and 10 vessels have been fitted with MAN Energy Solutions’ LNG burning energy unit. The methodology is in place to convert vessels to LNG power and DNV GL already has rules in place.

Will we see larger vessels such as VLCC tankers being converted to dual-fuel LNG power? Independent shipbroking house Affinity’s founder and managing partner Richard Fulford-Smith has long been a cheerleader of seaborne LNG, but he has his doubts regarding retrofits: “LNG retrofits on VLCCs will not happen,” he noted bluntly, citing the LNG tank arrangements and the financing involved in such conversions.

Still, this has not put off French LNG tanker designing Gaztransport & Technigaz (GTT), which has a solution in place for retrofitting LNG fuel tanks to VLCCs. Presenting at the 2019 Tanker Shipping & Trade conference, GTT’s product line manager Pascal Ta explained how one of the cargo tanks could be sacrificed to create the LNG tank. The LNG tank is constructed between two longitudinal bulkheads and is surrounded internally with GTT’s Mark III propriety insulation. The primary barrier prevents the steel hull from contact with the LNG and carries the structural loads. On the internal tank side of the insulation is the GTT waffle structure, which reduces sloping of the cargo and carries the stresses from the cargo during the voyage.

The converted tank is midway of the hull of the converted tanker to reduce hull stresses. For a tank of 14,000 m3, the tank will be around 27-m long. The converted tanker would also require piping and all other ancillary equipment associated with LNG dual-fuel.

It has been noted elsewhere that funding such retrofits might not be as problematic as first impressions suggest. Several years ago, when the IMO 2020 marine fuel sulphur cap was first proposed, many banks were doubtful that financing scrubber retrofits was possible. But since then, hundreds of scrubbers have been retrofitted – many financed by banks. It seems that if the business case makes sense, then the finance will be made available, which is good news for LNG retrofits. Indeed, the cyclical nature of shipping and the environmental pressures on the industry might, by 2030, conspire to make the conversion of a modern VLCC into LNG-power a very attractive proposition.

Related to this Story

Events

Maritime Cyber Security Webinar Week

International Chemical & Product Tanker Conference 2024

Marine Propulsion: Fuels Webinar Week

How enhanced connectivity is propelling maritime into the AI era

© 2023 Riviera Maritime Media Ltd.