Business Sectors

Contents

")

Sector downturn forces liftboat sales at distressed prices

The low-oil price environment and Covid-19 demand destruction have dealt a one-two punch to the liftboat sector, but its prospects could be buoyed thanks to offshore wind

Not surprisingly, liftboats, like most other offshore assets, have been significantly affected by the Covid-19 pandemic, low oil prices and reduced oil demand. “An already fragile sector has, over the last 12 months, been forced further into the floor,” VesselsValue (VV) head of offshore Rob Day tells OSJ.

Recent events have placed further downward pressure on valuations in the sector that started back in 2014/2015. Mr Day says several distressed sales at the latter part of 2020 and the start of 2021 illustrate the challenges liftboat owners face.

He cites how financiers forced Singaporean offshore owner Ezion to sell two modern liftboats from its fleet. These transactions in January saw Teras Conquest 7 (336-ft, built in 2015 by Triyards Ho Chi Minh) sold to Elite Point Pte Limited Singapore for US$13M. VV puts the current valuation of Teras Conquest 7 at US$18.06M.

In December 2020, Teras Fortress 2 (450-ft, built in 2015 at Triyards Ho Chi Minh) was sold to Virgo Shipping for US$22M; the current VV Value is US$21.45M. Teras Fortress 2 (and its sister Teras Fortress) are the largest liftboats by leg length (ft) in the world fleet and were contracted at about US$90M in 2012. Both Teras Conquest 7 and Teras Fortress 2 had a negative impact of liftboat values.

Looking at the price change for the five-year valuation for Milaha Explorer (295-ft, built in 2016 by Bohai Shipbuilding) and Mr Day says “over the last three years alone, the asset has lost about 50% of its value. As about February 2019, the VV value was US$38.57M, compared to a valuation of US$18.95M as of 16 February.”

: “A return to normal – whatever normal is? – looks likely to be closer to 2022/23” (source: Riviera)")

Middle East sale rumoured

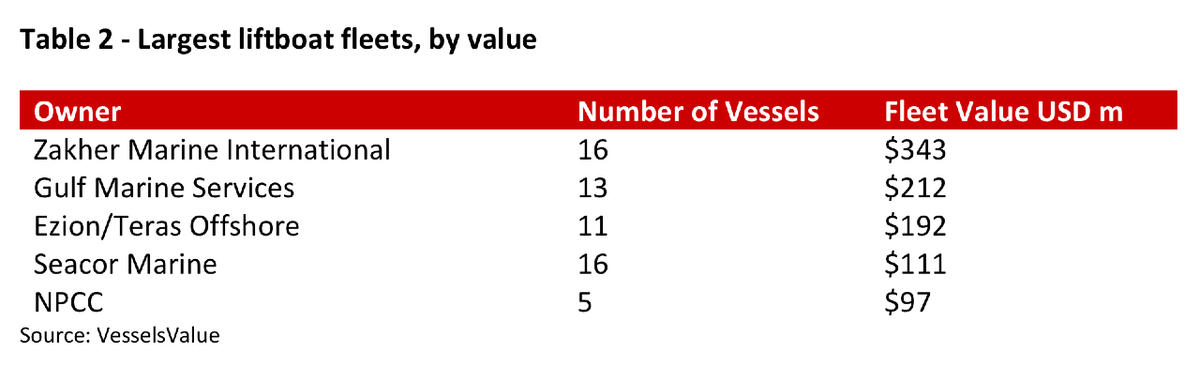

One large liftboat deal among Middle East offshore vessel owners could be looming. Rumours in the offshore market suggest that Zakher Marine Services have recently been in talks to sell its entire liftboat fleet to Abu Dhabi National Oil Company (ADNOC). Although there is no official confirmation of the deal, if it were to conclude, ADNOC would be purchasing a total of 16 liftboats, with an average age of three years old and a total value of US$342.8M.

Mr Day notes that brokers continue to market for sale a number of US-built liftboats, one of which is Seacor Influence (265-ft, built in 2009 by Boconco), with a VV value of US$4.65M. Several smaller US units in the 175-ft to 230-ft class range remain for sale, as many owners look to exit the market. However, they remain unsold as buying interest from both US- and non-US-based buyers remains low.

Low utilisation in US GOM

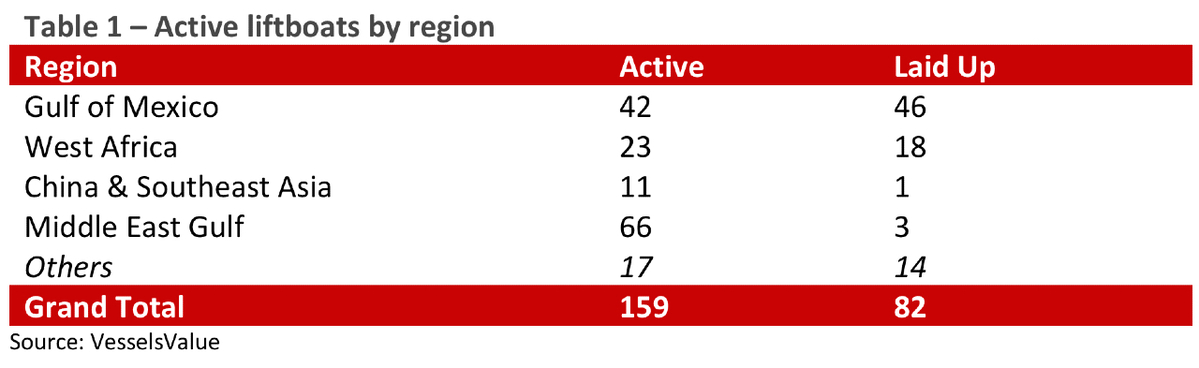

Using VesselsValue’s recency of AIS data, Table 1 shows the US Gulf of Mexico (US GOM) is suffering poor utilisation and high numbers of laid-up vessels. Of the fleet of 88 liftboats in the US Gulf, 46 have not signalled in more than eight weeks. In contrast, the Middle East, Asia and Southeast Asia show strong utilisation figures.

To enhance its offshore oil and gas and renewables valuation coverage, the UK-based ship and vessel valuations firm has expanded its coverage of liftboats. Entering the offshore market in 2016, VV launched automated values for about 11,000 offshore vessels covering: supply vessels (platform supply vessels, AHTS vessels, fast supply vessels); mobile offshore drilling units (MODUs), both jack-ups and floaters; and offshore construction vessels (OCV) – including multi-purpose vessels and dive support vessels. The valuations are often utilised by banks, insurers, brokers, vessel owners, managers and operators that have exposure in the offshore sector.

Mr Day says the addition of liftboat coverage by VV was a “logical next step” as it represents a key link between offshore oil and gas assets and the renewables sector to complete VV’s oil and gas portfolio and help it initiate steps to expand into the renewables sector.

He sees a challenging market ahead for the liftboat sector and the offshore market as a whole, weighed down by uncertainty caused by Covid-19 and country-phased lockdowns. “A return to normal – whatever normal is? – looks likely to be closer to 2022/23,” says Mr Day.

He cautions however, this could be optimistic given the new variant virus strains, with countries continuing to experience second and third waves of infection.

Offshore wind opportunities

It may not be all doom and gloom though, as Mr Day notes the liftboat sector could be buoyed by prospects in the growing offshore wind energy market. “Opportunity could ‘come a knocking’ for some liftboat owners,” he says. He thinks ageing offshore windfarms across Europe could generate opportunities for increased upkeep and major maintenance/component replacement.

“Offshore wind turbines typically have about a 20-year lifespan and with a large number of smaller turbines being installed from 2000 onwards, this could provide a steady workflow over the coming years for liftboats,” says Mr Day. “Equally, liftboats could provide a far more affordable turnkey solution for turbine installations compared to a full wind turbine installation vessel (WTIV).”

Outside of renewables, he feels there are some opportunities for larger liftboat units within the Middle East and Asia that could find work in alternative sectors, like civil engineering projects.

“[Smaller, older US GOM liftboats are] likely to continue to suffer as a result of poor overall market fundamentals and the continued pressure of Covid-19,” he observes. “Owners are remaining hopeful with the prospect of offshore wind in the US. However, there will be limited opportunities for these assets in this sector, due to the increasing size of turbines and European operator standards, resulting in most units being obsolete for tenders.”

“Opportunity could ‘come a knocking’ for some liftboat owners in offshore wind”

While the number of US-built liftboats is 50% larger than the internationally built fleet, the valuations are quite different. This is because liftboats built outside of the US are typically higher specification (DP1, DP2, SOLAS, larger crane capacity, larger deck area, etc), with larger leg length and have generally been built within the last five to eight years, according to Mr Day. “[This] creates a big difference between the asset values,” he says.

As a result, as of 16 February, the total US liftboat fleet value was US$281.62M, while the total fleet value of those built outside the was US$1.69Bn, according to VV.

VV - Coverage of liftboats

VV’s coverage of the liftboat sector will focus on three core services with live, fully automated current and historical market, demo and newbuild valuations for the entire liftboat fleet; a comprehensive fleet and commercial database with advanced search functionality; and live AIS and GIS mapping tools to track the world fleet with added analysis overlay functionality to incorporate all offshore (fields, wells, licenses etc) and renewables (windfarms, turbines, substations etc) GIS layers.

Plans call for full global fleet coverage, comprised of 247 liftboats, which will be categorised as ‘small, and ‘large’ liftboats. “Small liftboats,” explains Mr Day, “are mainly units in the US GOM and West Africa and large liftboats are those built or working in the Middle East, Asia and Southeast Asia.”

With prospects for offshore wind growing, VV anticipates further valuation coverage in the renewables sector, adding automated values for crew transfer vessels in the near future, says Mr Day.

Valuing liftboats with an algorithm

VesselsValue explains that its VV algorithm is a “transactional-based, five-factor model” which will impact a liftboat’s valuation.

These five factors are based on firstly, the type of liftboat, whether it is both self-elevating and self-propelled. VV says only assets that meet these criteria will be applicable to live valuations.

Secondly, the five factors are based on the features of the vessel and specification. For example, buyers will pay more for a vessel built at the most reputable yards compared to a similar vessel built at a less-established yard.

Thirdly, the age of a vessel, which VV explains is not simply a matter of depreciation by a fixed annual amount. “A vessel has a finite but unknown lifetime over which to generate earnings, and VV’s regression analysis commonly finds in the first few years of a vessel’s life the depreciation is not so steep. However, after five years its curve steepens until it’s nearing the end of its life, when the age depreciation tends to stabilise again,” says VV.

Fourthly, a liftboat’s size impacts its value. When it comes to the liftboat market, size is determined by leg length and measured in feet (ft). “Typically, as leg length increases the cost of construction increases,” says VV.

The fifth and final factor is earnings sentiment. VV explains that the best proxy for offshore earnings sentiment is an index derived from a long- and short-term rolling average of the Brent Crude price. The oil price is the prime driver for the offshore market, and effects vessel utilisation, charter rates and market values. The correlation has been tested historically.

VV head of offshore Robert Day adds, “The primary driving factor in the fluctuation of a vessel’s value is the S&P market.” These transactions are automatically fed into VV’s algorithm once confirmed. “The more recent a transaction, the greater its influence on the current prices, hence the importance in shipping of ‘last done’ deal.”

Related to this Story

Events

Shuttle Tanker Webinar Week

International Tug & Salvage Convention, Exhibition & Awards 2024

Responsible Ship Recycling Forum 2024

Offshore Support Journal Conference, Americas 2024

© 2023 Riviera Maritime Media Ltd.