Business Sectors

Business Sectors

Events

Contents

Register to read more articles.

")

Global LNG fleet to eclipse 1,000 vessels by 2026

By 2026, the global LNG fleet is forecast to exceed more than 1,000 vessels, propelled by the addition of 295 newbuilds on order, according to a leading shipbroker

A market overview released in January by Howe Robinson Partners forecasts 48 newbuilds will join the LNG fleet in 2023, 28 of which will have a capacity of 174,000 to 200,000 m3. Overall, LNG carriers with capacities of 100,000 m3 or more account for 285 of the 308 vessels on order – almost 93% of the orderbook at South Korean and Chinese shipyards. This newbuilding boom will grow the fleet by 25% from 2023 to 2026.

Many of these new vessels will be delivered into term charters which will keep the spot market tight, pointed out the shipbroker. “The number of uncommitted newbuilding vessels until the end of 2026 stands at less than 30,” said Howe Robinson Partners, noting, “A number of tenders for vessel delivery in 2026 could remove at least six further gas injection vessels.”

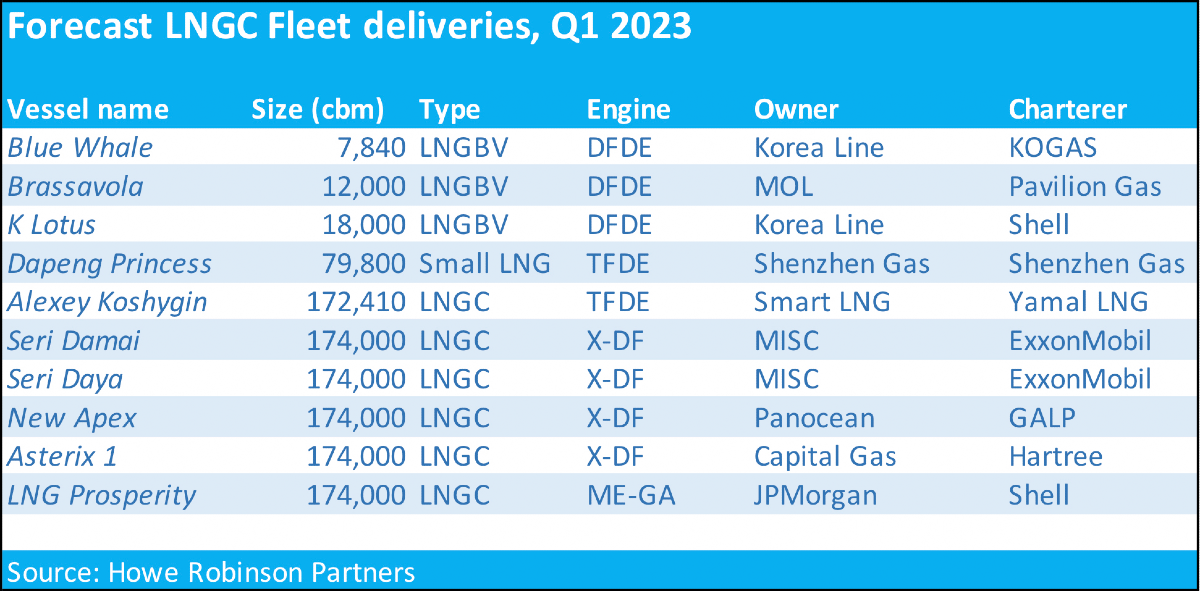

Howe Robinson Partners projects 10 LNG vessels will be delivered in Q1 2023, three of which will be LNG bunkering vessels, as shown in the accompanying table.

Overall, the current global LNG fleet is relatively young, with 69% 10 years of age or less. 80% of the fleet is fitted with membrane containment systems.

Four project FIDS

Besides global fleet development, Howe Robinson Partners forecast at least four LNG projects would face FIDs in Q1 2023, three in the United States and one in Mexico. The three projects in the US are: Energy Transfer’s Lake Charles LNG (three trains, capacity of 17.5 mta), Sempra’s Port Arthur, Phase 1 (two trains, capacity of 13.5 mta) and NextDecade’s Rio Grande, Phase 1 (three trains, capacity of 16.2 mta). Mexico Pacific’s Saguaro LNG (two trains, capacity of 9.4 mta) is the lone project in Mexico.

Several other projects could see FID later in 2023.

Sign up for Riviera’s series of technical and operational webinars and conferences in 2023:

- Register to attend by visiting our events page.

- Watch recordings from all of our webinars in the webinar library.

Related to this Story

Events

Maritime Regulations Webinar Week

Floating energy: successfully unlocking stranded gas using FLNGs and FSRUs

© 2026 Riviera Maritime Media Ltd.